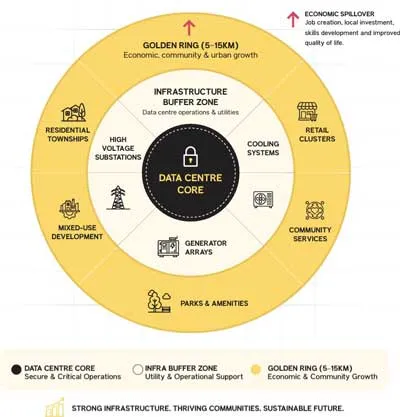

Data Centres May Drive 195 Mn Sq Ft Housing Demand by 2030

India’s expanding data centre ecosystem could generate demand for nearly 195 million sq ft of residential space by 2030, according to a report by proptech company Square Yards.The report estimates that the country’s proposed data centre pipeline of approximately 9,030 MW could create nearly 433, 000 jobs across supporting industries and services, strengthening housing demand in surrounding locations.Unlike conventional commercial developments, data centres attract investments in power infrastructure, fibre connectivity, logistics, commercial facilities and ancillary services. These investm..

CenturyPly Launches Total Cover Warranty for Furniture Costs

CenturyPly has launched Total Cover, a comprehensive warranty programme that reimburses furniture-related expenses arising from confirmed defects in its Club Prime and Architect Ply products within ten years of purchase.The cover extends beyond replacing defective plywood and includes the cost of laminates or veneers, adhesives, labour and transportation required to rebuild or repair the affected furniture.The company developed the programme after centralising customer complaints from across India around two and a half years ago. Its review found that customers were often more concerned about ..

LANXESS Explores New Markets for Iron Oxide Innovations

LANXESS is exploring new applications for its iron oxide products across batteries, catalysts, water purification and hydrogen storage as its pigments business celebrates its 100th anniversary.The company’s innovation team is conducting initial application tests and working with strategic partners to tailor products to emerging customer requirements. The initiative aims to take LANXESS iron oxides into new markets while strengthening its existing product portfolio.Battery materials represent a major area of focus. LANXESS is working across several project phases to develop iron oxides and ir..

Latest Updates