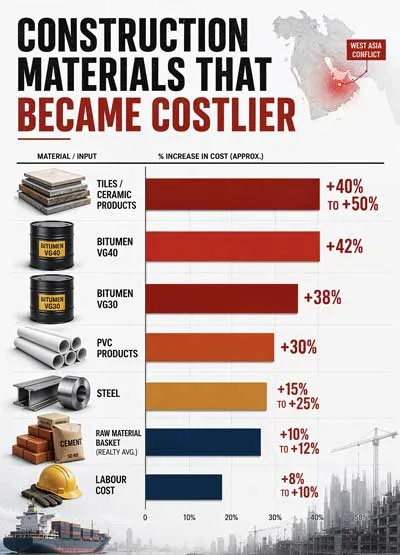

War in West Asia and the ensuing disruption of shipping through the Strait of Hormuz has impacted the entire world – and India is no exception. The country sources critical construction inputs like bitumen and LNG from the Gulf while rising global fuel prices, which have already driven up domestic wholesale diesel prices, bear adversely on logistics, a service with a wide impact on primary as well as secondary construction materials.“Volatility in global energy markets typically flows through to construction materials such as steel, cement and aluminium, as well as inputs like glass and tiles,” says Sudharshan KR, Chief Project Officer, Mahindra Lifespace Developers. “In addition, materials such as tiles and ceramics, copper, bitumen, resins and paints have also seen an increase.”Sudharshan projects overall construction costs in India to have risen by around 5-12 per cent as a result of the ongoing situation.“Steel and cement are under pressure because their production makes use of coke, coal and natural gas,” notes Virendra Vora, Promoter, Excel Infrastructure. “Their prices are up by nearly 40 per cent and supply is short.”Geopolitical tensions in the Gulf have driven up petcoke, coal and logistics costs, while potential rises in power and fuel and freight costs in the near term are likely to push up pan-India average cement prices by Rs 10-15 per bag during April-May 2026 compared to March 2026 levels, according to Anupama Reddy, Vice President & Co-Group Head, ICRA. While she believes that residential real-estate projects’ typical four to six-year lifecycle and built-in cost contingencies of 4-5 per cent of construction cost will give developers sufficient flexibility to absorb the transient input cost volatility, industry voices suggest they are not insulated from events in the Gulf.CW identifies the construction sectors most vulnerable to the ongoing situation, with an in-depth look at real estate and roads, and relief measures the Government can roll out.Who’s most affectedThe roads and ports sectors have emerged as the most impacted segments amid ongoing disruptions, avers Aniket Dani, Director, Crisil Intelligence.While the roads sector has been analysed in detail ahead, traffic and capacity utilisation at ports has been affected by route diversions. Petroleum, oil and lubricant (POL) products accounted for 28 per cent of overall traffic at Indian ports in fiscal 2025, half of which passed through the Strait of Hormuz, and have been impacted the most, he says. “Any sustained reduction in POL traffic is likely to reduce revenue, with the effect most visible at ports and terminals with higher exposure to liquid/bulk energy cargo such as Cochin Port, New Mangalore Port and Mumbai Port.”Among the least impacted sectors and sub-sectors, Dani counts water and sanitation (solid waste, treatment plants, sewage systems, water drainage systems), communication (telecom towers, networks and data centres), social and commercial infrastructure (education institutions, hospitals, sports infrastructure, tourism infrastructure), urban infrastructure, and renewables power transmission and distribution.“The building construction, power transmission and distribution, water and urban infrastructure sectors are structurally insulated from war-led shocks because they are minimally dependent on crude-derived inputs and largely rely on domestically sourced materials like steel, cement, aggregates and sand,” says Suprio Banerjee, Vice President & Co-Group Head, ICRA. However, if the conflict persists and energy costs remain elevated for multiple quarters, leading to an inflationary environment, selective price increases are possible. But, he says, “They are likely to be gradual rather than abrupt.”Given the differential impact of the situation, diversified EPC players are relatively better positioned to withstand sector-specific disruptions. “A broad-based order book mix provides a natural hedge against volatility in any single segment,” says Dani.Road construction woesWith bitumen imports from West Asian nations constituting ~33 per cent of India’s domestic consumption from April 2025 to January 2026, any supply disruption in that region would trigger material shortages and price volatility adversely impacting road and highway projects, where it is especially vital for resurfacing, overlays and maintenance works. Bitumen has witnessed the steepest hike in price among construction materials in India, affirms Banerjee. Prices of VG30 and VG40 grades, most commonly used for the construction of flexible roads, have increased by 38 per cent and 42 per cent, respectively, in the past four to six weeks, points out Dani.“Bitumen is our biggest concern as prices have increased sharply from about Rs 40,000 per tonne to nearly Rs 68,000 per tonne in a short period, which puts significant pressure on project costs, especially in fixed-price or long-duration contracts,” shares Satyanarayan Purohit, Vice President, Dilip Buildcon. At Dilip Buildcon, attempts are being made to manage the situation through efficiency improvements, better planning and cost control, he reveals. “But such steep increases are difficult to absorb entirely. It does affect margins and, in some cases, project viability.”If the ongoing disruption ends by April 2026, Dani expects the impact to be moderately to largely recoverable owing to temporary input cost pressure. In that instance, prices are expected to normalise in the next quarter (Q2FY27) to February 2026 levels. However, if the disruption only ends by June 2026, the impact will be more severe and eventually slow down the pace of construction, especially in the roads sector. Prices will remain elevated for a longer duration and align with the hike in crude prices.Banerjee expects “continued elevated bitumen prices to potentially erode ~200–300 bps of EBITDA margins for road focused EPC contractors, increasing the vulnerability of the road sector, which is already facing margin pressure from heightened competitive intensity and lower project awarding than other infrastructure segments.”To provide near-term respite to road contractors, the Roads Ministry has recently announced a set of working capital relief measures for a three-month period (April 1 to June 30, 2026), where road contractors will now receive payments on a monthly basis replacing the earlier milestone-linked billing framework. In addition, Banerjee explains, “The Ministry has announced the simultaneous release of price escalation claims along with monthly bills and reduction in price adjustment period to one month for key raw materials like cement, steel, bitumen and fuel to better reflect volatile input costs.”While the NHAIs cost escalation compensation mechanism for highway projects is a positive and timely step to ease developers’ cash flow pressures and improve liquidity, the current relief is for a limited period. If the volatility continues, Purohit underscores the need to extend or strengthen these provisions. “A more responsive and market-linked escalation mechanism in contracts – especially for EPC and HAM projects – would go a long way in balancing risk between developers and authorities. Continued support and flexibility in contracts will be important to ensure that project execution is not impacted.”Impact on realty Geopolitical tensions through March and early April 2026 have led to noticeable cost escalations across key construction inputs used in building construction.“Prices of metals, such as steel and copper, and PVC-based products have increased more than 10 per cent,” says Dr Niranjan Hiranandani, Chairman, National Real Estate Development Council (NAREDCO). Overall, he estimates raw material costs to have risen by approximately 10-12 per cent.Construction materials like steel, cement, aluminium, copper, PVC, tiles and polypropylene-based products, which had seen the most notable increase in prices of about 10 to 18 per cent over the past few quarters, have now additionally been driven by global supply dynamics, rising petroleum product prices and high insurance premium charges by freight operators because of the US-Iran conflict, adds Sanjay Dutt, CEO & MD, Tata Realty & Infra.Basic materials like steel, cement, PVC, aluminium and anything made from petrochemicals that go into construction are all getting more expensive, says Manoj Paliwal, Director, Viyaara Realty. “Recent industry figures show steel prices have jumped between 15 and 25 per cent. PVC is up even more, sometimes 30 per cent. Shipping is a lot pricier, too, thanks to higher insurance premiums and freight costs.”Further, reverse migration linked to cooking fuel-related pressures have firmed up labour costs, Dr Hiranandani estimates, by about 8-10 per cent.“Intermittent LPG supplies are impacting the availability of labour in colonies on construction sites,” agrees Dutt. Also, LPG shortages have impacted the production of tiles and sanitaryware; their capacity has been reduced by 30-40 per cent. A major concern for Vora is the gas shortage, which has severely impacted Morbi, India’s tile manufacturing hub as well as ceramic sanitaryware factories.“Many factories are either operating at reduced capacity or have nearly stopped production,” he says. “As a result, tiles and ceramic sanitaryware are currently in short supply. Developers are no longer able to choose tile designs or specifications freely, and are instead buying whatever limited stock is available from manufacturers. Prices of available tiles have surged by 40-50 per cent. This will impact project construction costs and property prices will see an upward trend soon.”Global supply chains taking a hit are another concern. While projects aren’t grinding to a halt everywhere, companies are definitely feeling the pinch. “Margins are thinner, budgets are being reworked and teams are adjusting timelines, especially when costs can’t budge because of fixed-price contracts,” says Paliwal.Dr Hiranandani points out that input cost volatility and labour constraints impact projects under construction as timeline pressures while real-estate projects in the finishing stages, nearing possession, have witnessed delays. At Tata Realty & Infra, project delivery in the next 12-24 months may not progress on schedule owing to the impact of the conflict.While execution timelines remain stable for Mahindra Lifespace Developers at present, Sudharshan says, “Contractor margins and procurement cycles will need to be managed because margin pressures are beginning to build, particularly for under-construction projects where revenues are already locked in and input and labour costs have risen by ~5-12 per cent.”At the Srishti Group, projects scheduled for delivery over the next 12-24 months remain firmly on track with a proactive procurement approach, diversified sourcing strategy and strong vendor partnerships helping to effectively mitigate risks and avoid any critical material shortages. “Any cost variations we are seeing are manageable and well within our planning assumptions,” says Kamlesh Thakur, Co-Founder & Managing Director.Dani expects residential projects slated for delivery over the next 12-24 months to more likely face delays than cancellations, given healthier developer balance sheets driven by premiumisation. Realty price calibrationDevelopers hit by supply disruptions have started budgeting for cost increases of 5 per cent or more, according to Paliwal. If these problems stick around, he expects property prices to follow suit and head up.If the situation persists for a month or longer, Shekhar Patel, President, CREDAI, agrees that it may begin to reflect in input costs, leading to a gradual impact on overall pricing. According to Dani, “Geopolitical cost pressures are more likely to compress developer margins than push prices higher but a prolonged blockade could increase cost pressure on developers for under-construction projects.”If the situation erupts again, Dr Hiranandani expects the cost pressures to remain elevated. In that case, developers who have absorbed the cost increases without immediate price revisions may need calibrated price adjustments, which may cause pain among buyers. While typical sale agreements don’t account for such unforeseen global disruptions, he sees recent events as possibly leading to more adaptive contractual frameworks in the future.Expectations for supportAs this shock came from outside the industry, companies are looking to the Government for help with costs, better access to funds and some flexibility in policies, says Paliwal, who endorses duty and tax cuts on essentials like steel, cement and petrochemicals to take the edge off rising global prices.“A stable policy environment is critical, so continued focus on infrastructure spending will help sustain demand across the sector, while rationalisation of duties on key raw materials, where required, can provide some relief on input costs,” agrees Sudharshan. “Ensuring smoother supply chains, faster approvals and adequate liquidity will also help developers manage working capital more efficiently during periods of volatility.”As long wait times eat into budgets and freeze up fund flow that could be put to work sooner, speeding up approvals would beneficial, adds Paliwal.Pushing for more domestic production of key materials would help as well. “If the Government leans harder into schemes like PLI, the industry wouldn’t have to rely so much on imports, which are often largely dependent on global supply,” he continues. “Continued emphasis on incentivising domestic manufacturing of key construction materials, along with sustained investments in infrastructure, will further enhance supply chain reliability,” adds Thakur. “Focused skill development initiatives to improve both the quality and availability of labour would also provide meaningful support.”As developers are already facing shrinking profit margins, Vora says government intervention to ensure that RBI improves liquidity and keeps interest rates stable is also important.Additionally, Dutt proposes relaxation in RERA completion timelines and project costs by way of tax rebates for real-estate developers, saying government regulators must thoroughly evaluate the conflict-imposed additional cost burden on real-estate developers and allow them appropriate relief on cost and time so that end customers don’t suffer. “We advocate expanded incentives, faster approvals, improved logistics and the promotion of precast techniques, bolstered by India’s resilient 7 per cent growth outlook, to sustain strong housing demand and sector momentum.”If geopolitical tensions hold steady, Dutt expects government measures to help stabilise prices in the next quarter, while de-escalation would accelerate moderation. “Stabilisation would position us well for continued execution,” he says. Especially, fuel cost stabilisation would be a key lever in easing overall cost pressures across the value chain.While the industry has a reputation for bouncing back, Paliwal points out that times like the present show just how deeply construction is now tied to global politics. “Developers can’t ignore the ups and downs in energy, raw materials and the tangled web of international supply chains; it’s time they strategize accordingly because volatility isn’t going away anytime soon.”Can force majeure provide relief?In the case of Energy Watchdog vs. Central Electricity Regulatory Commission (CERC), (2017) 14 SCC 80, India’s top court ruled that there must be “real reason” and “real justification” to invoke a force majeure clause, irrespective of whether the trigger is war, a catastrophe, riots, government acts leading to the expropriation or acquisition of the contractor’s rights or a change in law, etc.In the present instance, the trigger is the hike in fuel prices as a result of the war in the Middle East. War-driven price hikes inevitably slow down construction activity as companies grapple with cash-flow constraints, procurement delays and renegotiation of subcontracts. Ensuing time overruns expose contractors to claims of liquidated damages under their contracts.Still, the onus is on construction companies to assess the prevailing condition and identify whether it is likely to affect their ability to perform their obligation, if bona fide attempts have been made to prevent the effect or mitigate any losses, if the other party has breached any obligation and if compliances have been fulfilled for invoking a force majeure clause, explains Sadiqua Fatma, Senior Partner, Legacy Law Offices, LLP.Essentially, “construction companies cannot invoke a force majeure clause mechanically, which poses a considerable burden on them,” says Fatma, “especially when the price hike does not entirely prevent performance but makes it commercially ruinous.”Another challenge, she says, “is that construction contracts in India don’t contain adequate clauses to absorb sudden and severe external shocks such as war-driven commodity and fuel price escalations.” What would help, Fatma says, is the Ministry of Finance issuing a clarifying circular or policy direction in the context of the ongoing war and its economic consequences, specifically addressing the spike in fuel, steel, bitumen and other construction inputs, saying that the ensuing disruptions to government procurement contracts would be treated as a force majeure event. A similar clarifying circular had been issued in February 2020, in the early days of the COVID-19 pandemic.“A clarifying circular or policy direction would provide a uniform standard, reduce litigation and guide arbitral tribunals in adjudicating force majeure claims to prevent a multiplicity of conflicting decisions being rendered by different arbitral panels across the country,” in her view. “Calibrated government intervention through policy circulars, price variation mechanisms, fiscal relief, proactive dispute resolution and long-term legislative reform can substantially alleviate the distress caused by war-driven price hikes.”Additionally, the Government should direct its agencies to proactively grant construction companies reasonable extensions of time on ongoing projects without imposing liquidated damages for delays attributable to war-related supply disruptions and price hikes, adds Fatma. “Doing so would protect a contractor already suffering due to macroeconomic forces beyond its control from being further penalised by the levy of contractual damages.”All of these measures, however, may not help companies with private-sector contracts. “A lot of subjectivity is woven into the force majeure concept,” according to Manish Garg, CEO, Interarch Building Solutions. While the force majeure clause is written into all Interarch Building Solutions contracts the current conditions technically and legally don’t qualify to invoke it because India isn’t at war, and even when the Government declares force majeure, it is only for their contracts. According to Fatma, “The government must recognise that the infrastructure sector is the backbone of national development and its collapse or financial impairment due to geopolitical events beyond the sector’s control could have cascading consequences for public welfare and economic growth.”Unreasonable steel prices and availability issuesWhile steel prices have moved up by almost 25 per cent since January, essentially, the price rise started before the war broke out. That said, Manish Garg, CEO, Interarch Building Solutions, a provider of turnkey pre-engineered steel building solutions, informs, “Both downstream steel prices and availability became a bigger issue after the war started due to gas availability issues.”Metals have seen the most movement so far, with steel prices rising sharply in certain segments, alongside increases in aluminium and logistics costs, agrees Sudharshan KR, Chief Project Officer, Mahindra Lifespace Developers.At Interarch Building Solutions, availability is largely being managed by outsourcing from multiple channels, advance ordering and by changing the ordering cycle to N+3 instead of N+2. However, higher steel prices pose challenges on working capital and managing inventories. “Customers understand the situation and are adjusting prices wherever possible to absorb the impact,” according to Garg. Consequently, the order prices in many Interarch Building Solution orders are variable because they are linked with steel base pricing so that steel price increases are passed on to the end customer on a 1:1 basis.Further, he emphasised upon the need for the Government to control steel pricing. Anti-dumping duties introduced by the Government to protect the domestic steel industry must be abolished to bring prices in line with international levels, Garg believes. “I don’t see any reason for steel prices to have increased as they have.”Gulf’s loss, India’s gain? War triggers gradual return of labourBefore the war in the Middle East, India’s new labour codes had led to a moderate increase in the overall cost of labour, primarily owing to expanded social security contributions, revised definitions of wages and higher compliance requirements for employers, says Kishor Kumar TK, Director, National Labour Cooperative Federation of India, and Chief Project Coordinator, Uralungal Labour Contract Cooperative Society. “While these reforms enhance worker protection, formalisation and long-term welfare, they had also raised short-term cost pressures.”With conflict breaking out in the Middle East, labour markets across GCC countries have been moderately impacted, according to him. “While there is no evidence of large-scale layoffs yet, recruitment has slowed, projects have been delayed and job uncertainty has increased, particularly among low-skilled migrant workers. India is witnessing a gradual, early-stage return of workers, largely through contract completions and deferred migration rather than mass repatriation.”“So far, the flow of returning workers from the Gulf has been slow and steady, not a big wave,” agrees Manoj Paliwal, Director, Viyaara Realty. “While this return has helped a bit, it isn’t a long-term solution. Of course, labour coming back for good could actually help steady labour costs and make it a bit easier to get projects done on time.”Returning labour from the GCC region has provided modest relief to the domestic construction ecosystem, according to Kamlesh Thakur, Co-Founder & Managing Director, Srishti Group. “We have observed improved availability of skilled and semi-skilled workers.”- CHARU BAHRI