At the recently held RAHSTA Round Table on 29th April in Pune, and earlier during our webinars for Cement Expo by Indian Cement Review and by

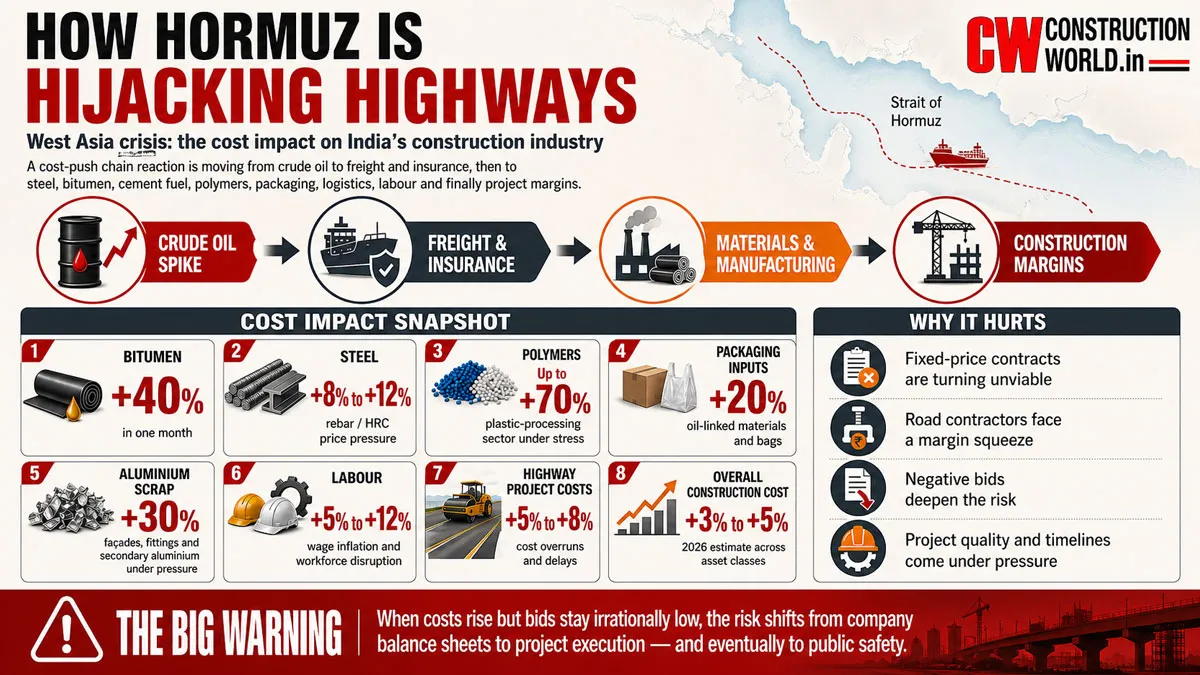

FIRST Construction Council on manufacturing construction equipment for the world, one thread lay common: the industry is being subjected to a cost-push chain reaction moving from crude oil → freight/insurance → steel, cement fuel, bitumen, polymers, packaging, logistics and finally project margins. Indeed, the West Asia crisis caused by the war and the Hormuz Strait blockade, which does not directly concern us, has turned around and hit us. If the war prolongs, it will hurt us even more.

Bitumen has jumped by over 40%, and steel makers have also hiked prices. For steel, raw materials such as scrap and coking coal remain irregular due to supply chain disruptions and logistical challenges. LNG shortages are particularly affecting small and mid-sized steel manufacturers reliant on gas-based processes — 65% of ArcelorMittal’s 9 mtpa capacity is dependent on gas-based direct reduced iron. LPG shortages are disrupting stainless-steel processes. Further, India imports around 90% of its met coal requirements, largely from Australia, which is now being affected by global supply and price volatility.

Prices of polymers have gone off the charts, rising by up to 70%, setting the stage for a collapse of the plastic-processing sector in several states, including Odisha, with more than 50% of the units halting production. This will hit the production of PVC, CPVC, conduits and electrical materials.

Cement and building-material suppliers face higher bagging and dispatch costs, which will lead to an increase in cement prices. Aluminium façades and fittings are facing an additional burden, with scrap prices rising by 30%. India, one of the world’s largest aluminium scrap importers, produces nearly half of its 4.2 million metric tonnes of aluminium through its secondary sector, which relies essentially on imported scrap. Labour supply has also been affected, as the voter turnout in West Bengal shows that many workers from the state returned home to vote. Initial LPG shortages also sent many workers back to their villages.

Given the rising costs, road contractors have been severely impacted. Government relief has been introduced for some compensation for the April–June quarter. Despite the thin margins this sector works on, it is alarming to see that contractors are fighting a pricing war. Bids revealed over the last few months show that contractors are quoting up to 45% lower than the estimated cost prepared by the issuing authority. Resultantly, it has become commonplace to see bids of up to minus 30% and beyond for most tenders. This is alarming for three reasons:

- Why is the issuing authority accepting such bids? Are they so unsure of their calculations that they would rather blindly believe that the negative bid factors in all their specifications?

- How will the contractor complete the project? Will the contractor be able to absorb the losses, or will his organisation collapse?

- Would users feel safe using the built structure, given that the contractor would have had to compromise somewhere to make up for the deficit?

Amid all this stands the question of an independent third-party audit — a practice that has no real sanctity in the current situation. If we are spending 3% of our GDP on infrastructure, it is essential that we deploy this investment well. We need a Comptroller & Auditor General for Infrastructure to be established, serving as a watchdog for quality. This will serve us well when there is negative bidding and also in projects like the Dwarka Expressway, where we have seen exorbitant spending.

The conversation about India’s RAHSTAs is gaining momentum. We are introducing a Highway Construction Masterclass at the

RAHSTA Expo on July 8–9, 2026, at Jio World Convention Centre. It will be the best place to attend a masterclass that will serve as a refresher course, set amidst an exhibition showcasing construction equipment, materials, technologies and products, while also enabling learning from industry stakeholders, researchers and academicians. Look out for page … and register before seats run out!

________________________________________